Capitalize Or Expense Carpet

When To Expense Vs Capitalize Costs And Benefits Of Cost Segregation Withum

Pin By Ashley Huff On Keepin It Clean In 2020 Cleaning Hacks House Cleaning Checklist Clean House

How To Google New Classroom Computer Internet Technology Poster Classroom Motivational Posters Classroom Computers Technology Posters

Recapitalization Capital Renewal What S The Number Tradeline Inc

Should I Expense Or Capitalize Purchases

Https Www Kbkg Com Handouts Kbkg Repairs Decision Tree Pdf

Maintenance expenses are used as an expense in full the year they occur.

Capitalize or expense carpet.

Can You Capitalize It As Ppe Or Not Ifrsbox Making Ifrs Easy

Block Letter Font On Microsoft Word Block Letter Fonts Lettering Fonts Block Lettering

Printable Master House Cleaning List Etsy In 2020 House Cleaning List Cleaning List Cleaning Hacks

Capitalize Or Expense Building Improvements Nonprofit Accounting Academy

What Are Fixed Assets A Simple Primer For Small Businesses Freshbooks Resource Hub

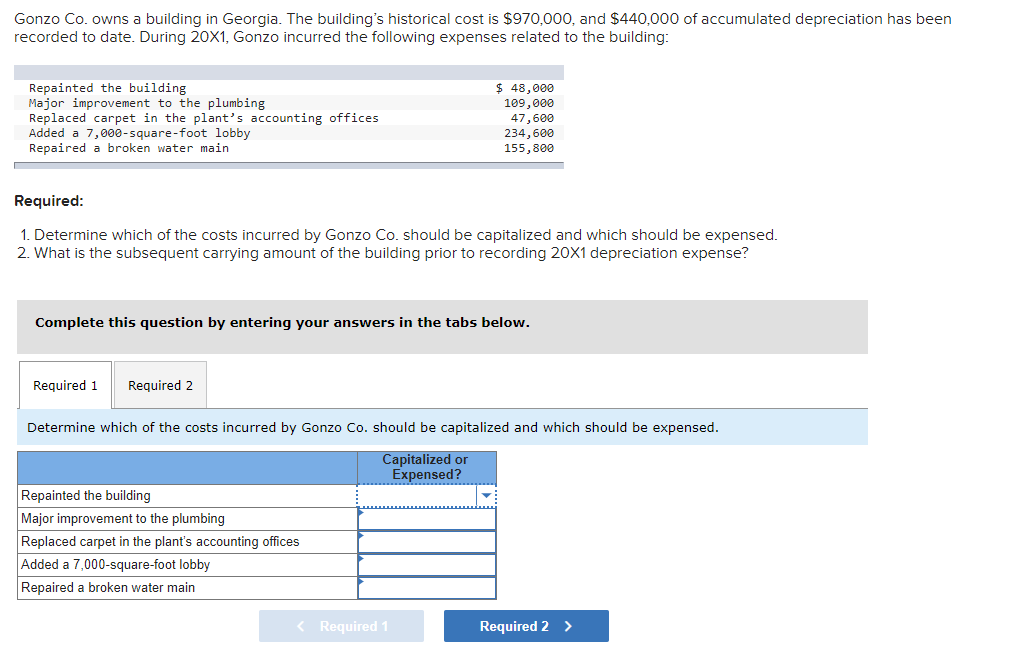

Solved Gonzo Co Owns A Building In Georgia The Building Chegg Com

When And What Should A Small Business Capitalize

Articles Leasing Expenses Above The Line Or Below The Line Expenses And Does It Matter Part 1

Flipping Houses Is Not Easy On Your Next House Flip Ask Yourself These 7 Questions To Save Yours Real Estate Investing Books Real Estate Tips Investing Books

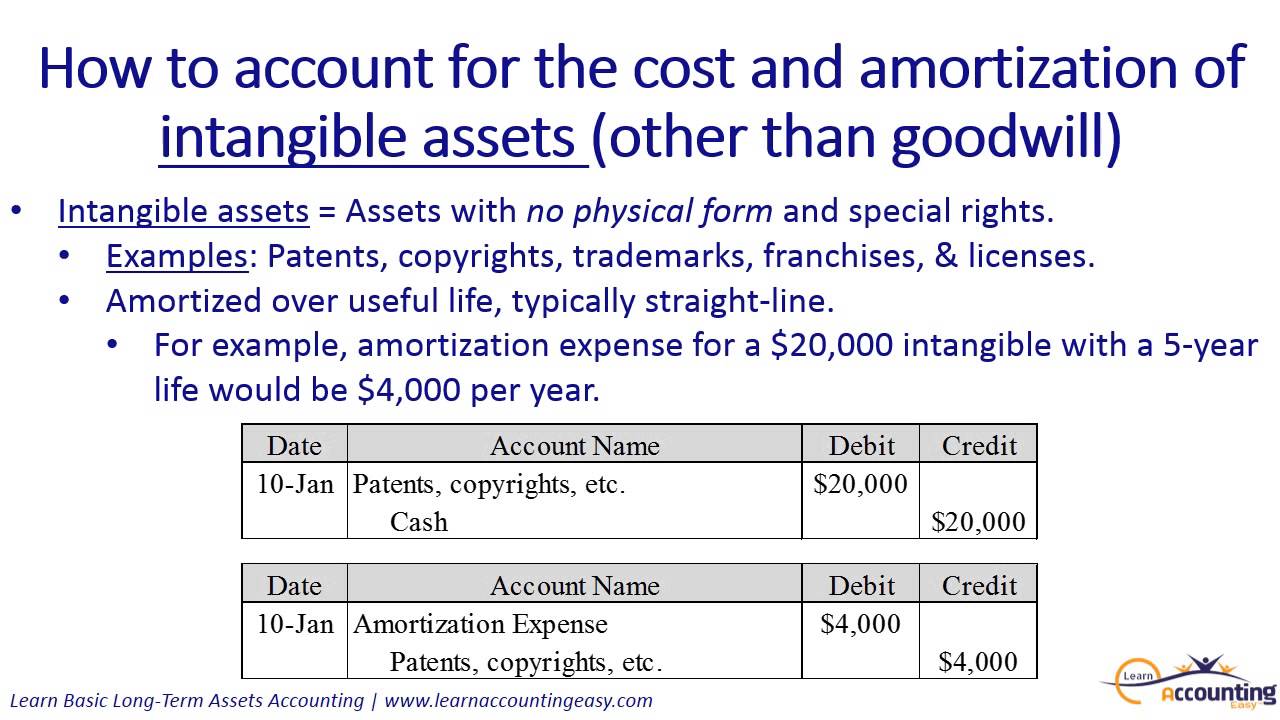

Intangible Assets Financial Accounting

Capital Expenditures The Ultimate Guide To Managing Capex In Companies

Millennials Go Minimal The Decluttering Lifestyle Trend That Is Taking Over Lifestyle Trends Minimalism Traditional Trends

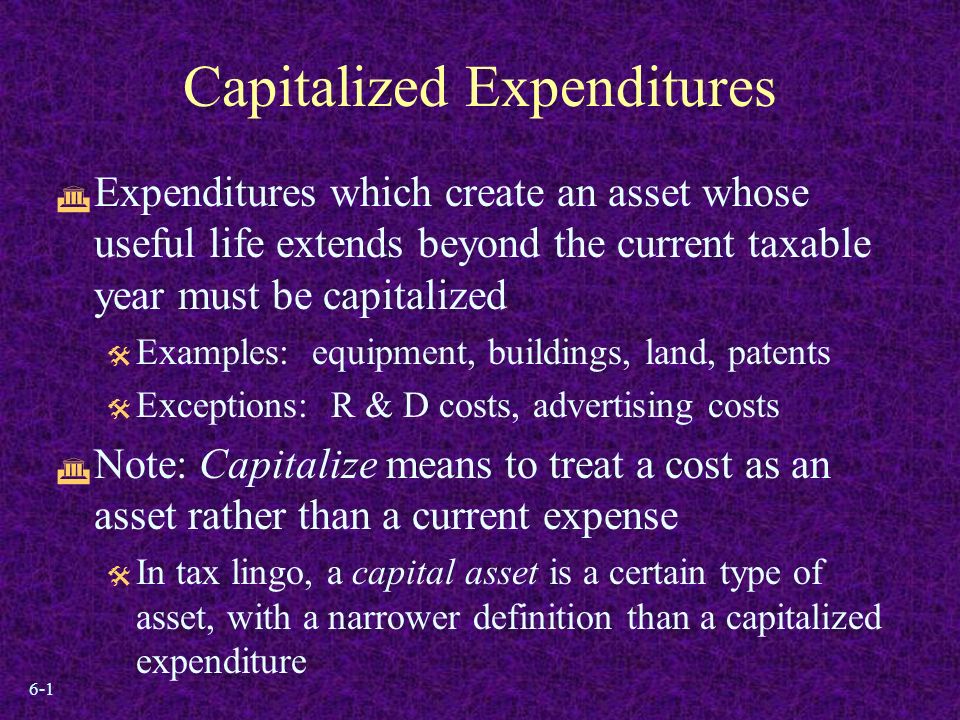

6 1 Capitalized Expenditures Expenditures Which Create An Asset Whose Useful Life Extends Beyond The Current Taxable Year Must Be Capitalized Examples Ppt Download

How To Make Beautiful Brown Paper Bag Floors Paper Bag Flooring Brown Paper Bag Floor Diy Flooring

Daily Driving An Ls Swapped Bavaria Getting Acquainted Ls Swap Engine Swap Dream Cars

Capital Assets University Of Colorado

Https Www Mscpaonline Org Writable Committee Updates Document Repair V Capitalization Davidfabian Pdf

How Uber Uses Data To Improve Their Service And Create The New Wave Of Mobility The New Wave Marketing Insights Social Media

3

Investor Presentation

Maintenance Or Capital Improvement What Is The Difference Why Does It Matter Heirloom Property Management Duluth Mn

Http Www Usg Edu Gafirst Fin Training Docs Final Capital Assets Bpm Updates Pdf

Exv99w1

Capital Expenditure Vs Repairs And Maintenance Keyrenter Denver

Source : pinterest.com